Economy

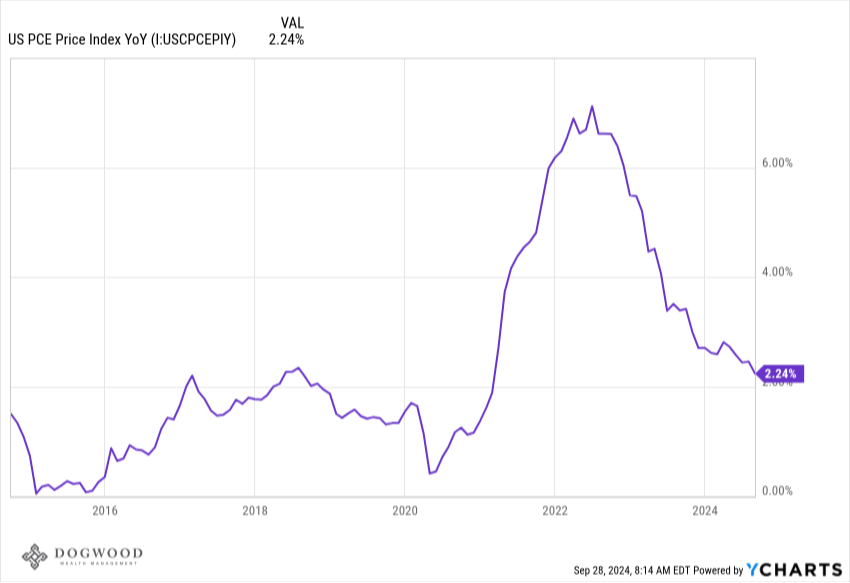

Coming off a week that saw the Fed lower interest rates for the first time since the pandemic, attention was on the Fed's preferred gauge for inflation, the personal consumption expenditures (PCE) index. By that measure inflation cooled to 2.2%, lower than expected going in to Thursday's report. In other economic news, weekly claims for unemployment insurance dipped to a 4-month low. Those two data points suggest the Fed was right to cut last week by 0.5%. We'd like to continue to see moderating inflation (which is currently near the Fed's target) alongside a stable labor market. Moving ahead, the Fed will meet twice more before the end of the year (November 7 and December 18). The market is currently pricing in at least 2, possibly 3 or 4, additional rate cuts.

We've been asked a lot about our thoughts on the upcoming election and the impact on the markets and/or the economy. While we don't want to downplay the significance of any election for a variety of reasons, I did hear an interesting analogy about the impact of the President on the markets. Some of you have already heard this, but it bears repeating, and it's apropos with the Royals clinching a playoff berth last night. There's an argument that can be made that the President has about as much impact on the markets as the manager of a baseball team has on the impact of their team's winning record over the course of a season. That is, the manager may impact the outcome of a game hear or there, but for the most part, the players on the field will determine the outcome of a game.

Markets

The S&P 500 rose 0.6% this week in a fairly calm week of trading. The markets continue to digest the Fed's latest move as we enter an era of declining rates. The S&P made three new all-time highs this week, but was slightly outperformed by it's equal-weight counterpart. That's a good sign of broad participation, not just a handful of names moving markets higher. We still have a whole 3 months to go before we close out the year, but to date, the market's returns have far exceeded that of most Wall Street analysts. The S&P 500 is now 20% higher than it was at the start of the year, and we've got a pretty good economic backdrop for the rally to continue. Earnings season is right around the corner so we'll soon have much more to talk about with respect to those "players on the field" we referenced above.

What We're Reading

- China Is Assembling an Economic Bazooka - WSJ

- Understanding Interest Rate Cuts - Dogwood Wealth Management

Have a great weekend.

Dogwood Wealth Management