Economy

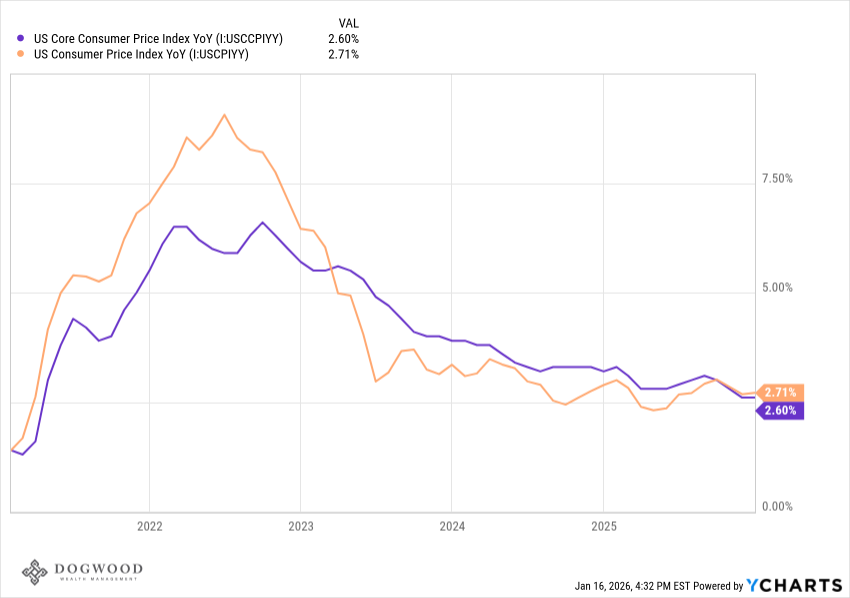

Inflation rose less than expected in December, coming in at an annual rate of 2.7% (2.6% excluding food and energy prices). This weeks consumer price index (CPI) report showed that, while inflation doesn't appear to be reaccelerating or getting "hotter", it remains above the Fed's stated target of 2%. Still, core CPI was above 3% as recently as August, so it's at least moving towards the Fed's target.

With respect to the labor market, the 4-week rolling average of the number of Americans that filed for unemployment insurance in the last week declined to the lowest level in 2 years - further evidence that while companies may not be rushing out to hire new employees, they aren't in a hurry to slash jobs. We remain in a "slow hire, slow fire" job market.

When observing the balance between inflation and the labor market, it seems as if Wall Street expects the Fed to hold rates steady at the next Federal Open Market Committee meeting on January 28. An added layer of drama is the political pressure being imposed on the Fed by President Trump to reduce interest rates. Now under a criminal investigation, if the Fed were to cut rates, it could appear as if they are giving in to the pressure. If they hold rates steady, there will undoubtedly be calls that they are acting in defiance. An unfortunate set of circumstances, but Jerome Powell will be Fed Chair for (no more than) 3 more FOMC meetings before President Trump appoints a new Fed Chair. On Friday, President Trump seemingly made Kevin Warsh the frontrunner for the soon to be vacated Chair position by telling Kevin Hassett he wants to keep him where he is (Director of the National Economic Council).

Markets

The S&P 500 fell slightly this week by 0.38%. The major banks kicked off earnings season, and part of the reason for the lackluster response was due to President Trump's proposal to cap interest rates on credit cards at 10%. While you may or may not agree with the proposal, it is understandable why financial companies wouldn't be thrilled about that and how it could impact future corporate profits. On top of that, the whole Fed/Powell criminal investigation story didn't inspire much confidence in the market this week. Still, earnings season starts to get hot and heavy next week, and according to FactSet, earnings are expected to grow by more than 8% for the fourth quarter.

We are (understandably) getting asked frequently what we think the market will do in 2026. While the honest answer is "who the hell knows" it does serve as a good reminder to have a diversified portfolio, and if you haven't rebalanced your accounts in a while, it may be a good time to do so. We've seen back-to-back-to-back years of low 20's and a high teen return in the markets. This isn't a call for a bear market, but it is a good moment to reflect on your risk appetite, and on how you were feeling in 2022 as the market grinded lower for months on end, or as recently as April 2025 when the S&P 500 lost 10% inside a week as tariffs were announced.

What We're Reading

- The Dark Side of Financial Education- Safal Niveshak

- Does This Bull Market Have a Divergence Problem?- JC Parets

Have a great weekend.

Dogwood Wealth Management