Economy

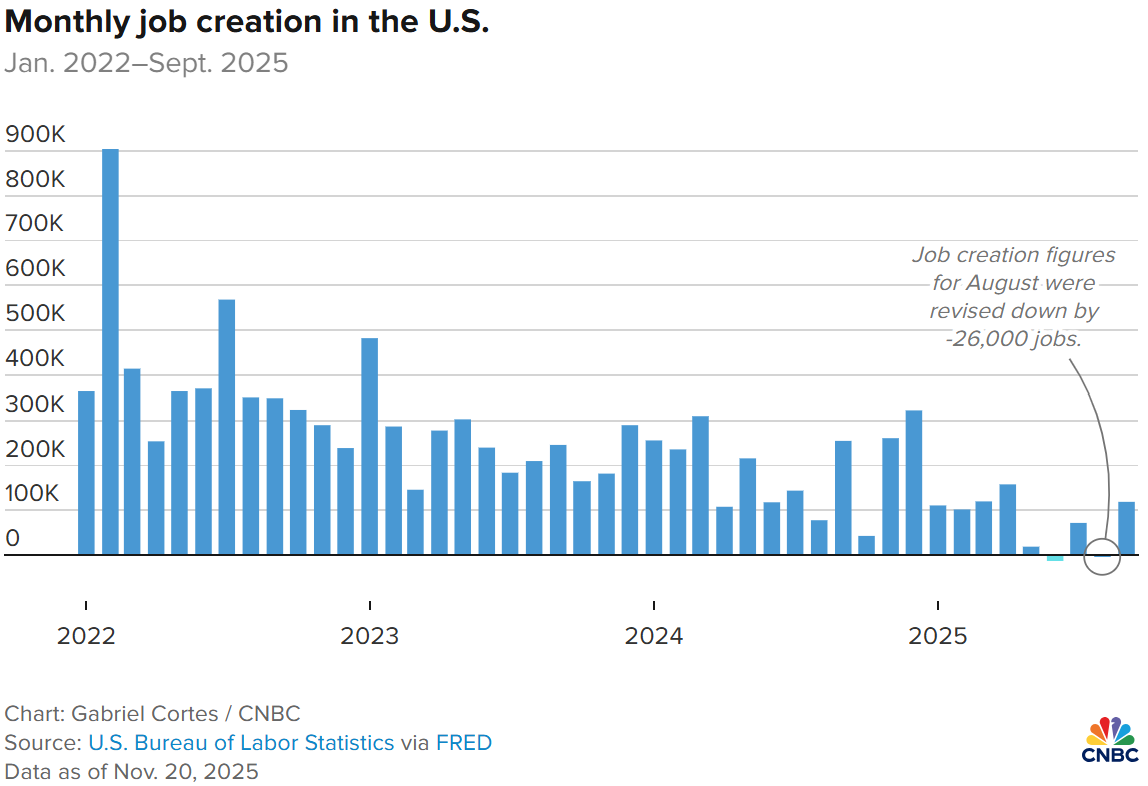

The Labor Department announced that it was cancelling the release of several economic reports, including the October jobs report as well as the October inflation report. It did, however, publish a much delayed September jobs report which showed the economy added 119,000 jobs for that month, a nice bounce back from August's decline of 4,000 jobs. The unemployment rate rose to 4.4%, the third consecutive increase from the June reading of 4.1%. The November jobs report will be released, just a bit later than previously scheduled as the department looks to get back on track following the government shutdown.

This unfortunately means that the neither the jobs data nor the November inflation report won't be published until after the Fed meets on December 10 to announce what they'll do with interest rates. A week ago, the bond market was giving us 50/50 odds of a rate cut in a few weeks, but on Friday those odds shifted to a 70% likelihood of a cut. This change in expectations was largely due to New York Fed President John Williams' speech, where he remarked seeing "room for a further adjustment in the near term..."

Markets

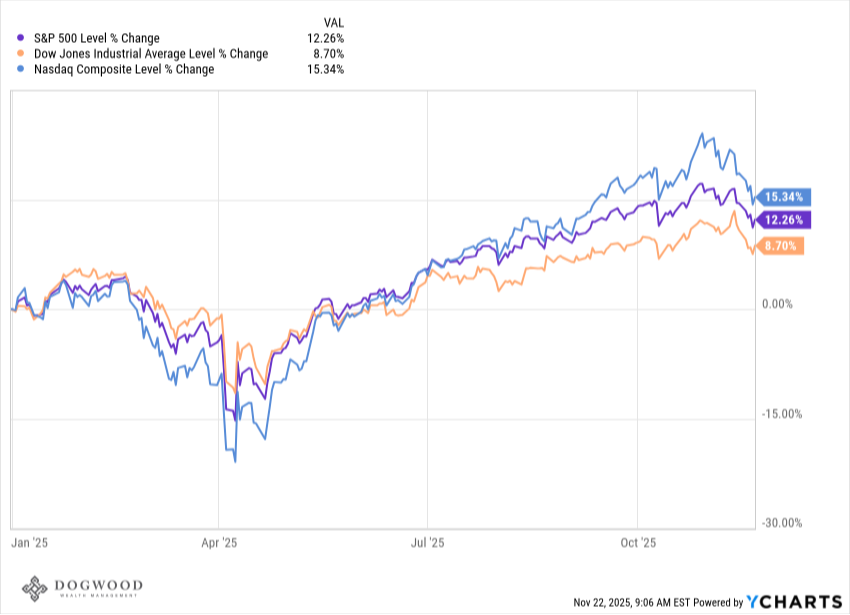

Despite Friday's broad rally, the S&P 500 posted a decline of nearly 2% this week. Even with Nvidia delivering a phenomenal earnings report, the selling pressure continued to inflict pain on the market, especially in tech stocks. With the last of the Magnificent Seven stocks having reported, we've nearly closed the books on the third quarter earnings season. Even with lofty expectations entering this season, companies surprised to the upside at an above-average rate, according to FactSet. The S&P 500 reported the highest revenue growth in 3 years, and the growth occurred not just in tech or AI stocks, but in all eleven sectors of the market.

Even with the recent 5% pullback, the market is still up 12% for the year. Now that earnings season is behind us, we will wrap up the year with another Fed meeting, a few significant economic reports, and a holiday-shortened trading schedule. Whether or we see a December "Santa Claus" rally may hinge on what we hear from Jerome Powell and the FOMC in a few weeks.

What We're Reading

- Thinking About 2026- Ryan Detrick

- Retirement is a Sprint, Not a Marathon- Fritz Gilbert

Have a great weekend.

Dogwood Wealth Management