Economy

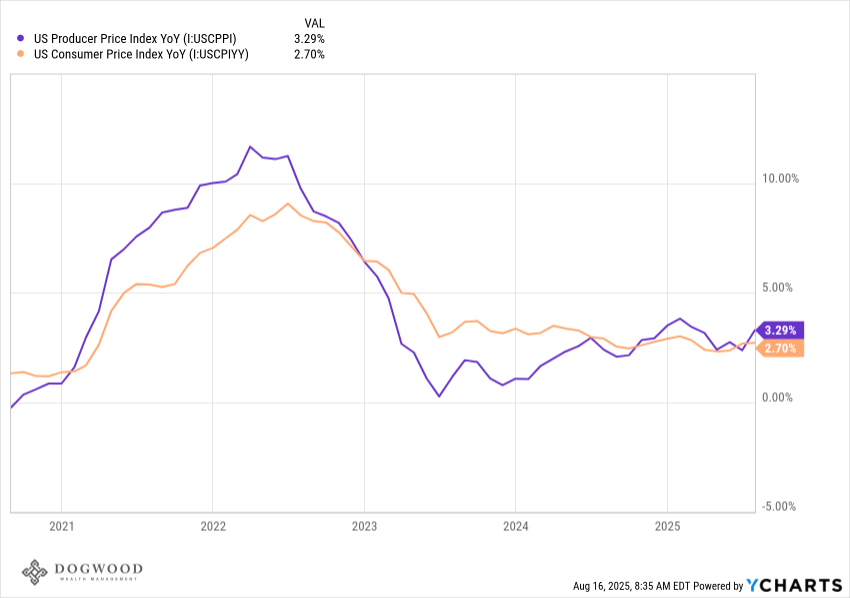

Inflation rose in line with expectations for the month of July, with the consumer price index (CPI) rising by 0.2%. Core prices, excluding food and energy costs, rose a bit more by 0.32%. A decline in energy prices helped keep the overall rate of inflation down. The largest contributors to inflation last month were shelter costs (rent was up 0.3%), medical care services (up 0.8%), and transportation (airfare jumped by 4%). While consumer prices (the prices you and I spend money on) remained tame, producer prices (the prices companies pay for goods and services they sell to you and I) took a huge jump last month. The producer price index (PPI) rose by 0.9%, the largest monthly increase since March 2022. The two reports might suggest that tariffs are impacting prices that companies are paying, but that the price increases are being eaten by companies at this stage, and not yet fully passed through to the end consumer. Whether or not that trend remains is to be seen. By the end of the week, the CME FedWatch Tool showed the market is pricing in a greater than 90% chance of a rate cut at next month's Fed meeting. We may get a glimpse into how they are feeling about the last disappointing jobs report and mixed inflation reports this week when the Fed meets in Jackson Hole for its annual symposium.

Markets

The S&P 500 hit fresh all-time highs this week, climbing 0.94% as the market reacted to the latest inflation and corporate earnings reports. I didn't mention the retail sales report in the section above (sales were up 0.5% last month) but we'll get a good pulse check next week when mega retailers Target and WalMart report on Q2 earnings. Perhaps the most significant single company in the world right now, Nvidia, has yet to report (we'll hear from them the week after this), but by now we've heard from most of their customers. The second quarter's earnings expectations as a whole had been reduced by forecasters going in to earnings season, but the actual performance of companies has been remarkably above those lowered expectations. So far we've seen double-digit growth in corporate profits for the quarter in which analysts expected to see something like 4%. However, critics of the market will point to how large of an influence the top 10 or so companies have on the index. It is true, the market has never been as concentrated at the top as it is today. The top 10 companies by size (market cap) make up nearly 40% of the S&P 500. Said another way, the top 25 companies combines are larger than the next 475 companies in the index.

What We're Reading

- Can the Stock Market Cause a Recession? - Ben Carlson

- America's Stock-Market Dominance is an Emergency for Europe - WSJ

Have a great weekend.

Dogwood Wealth Management