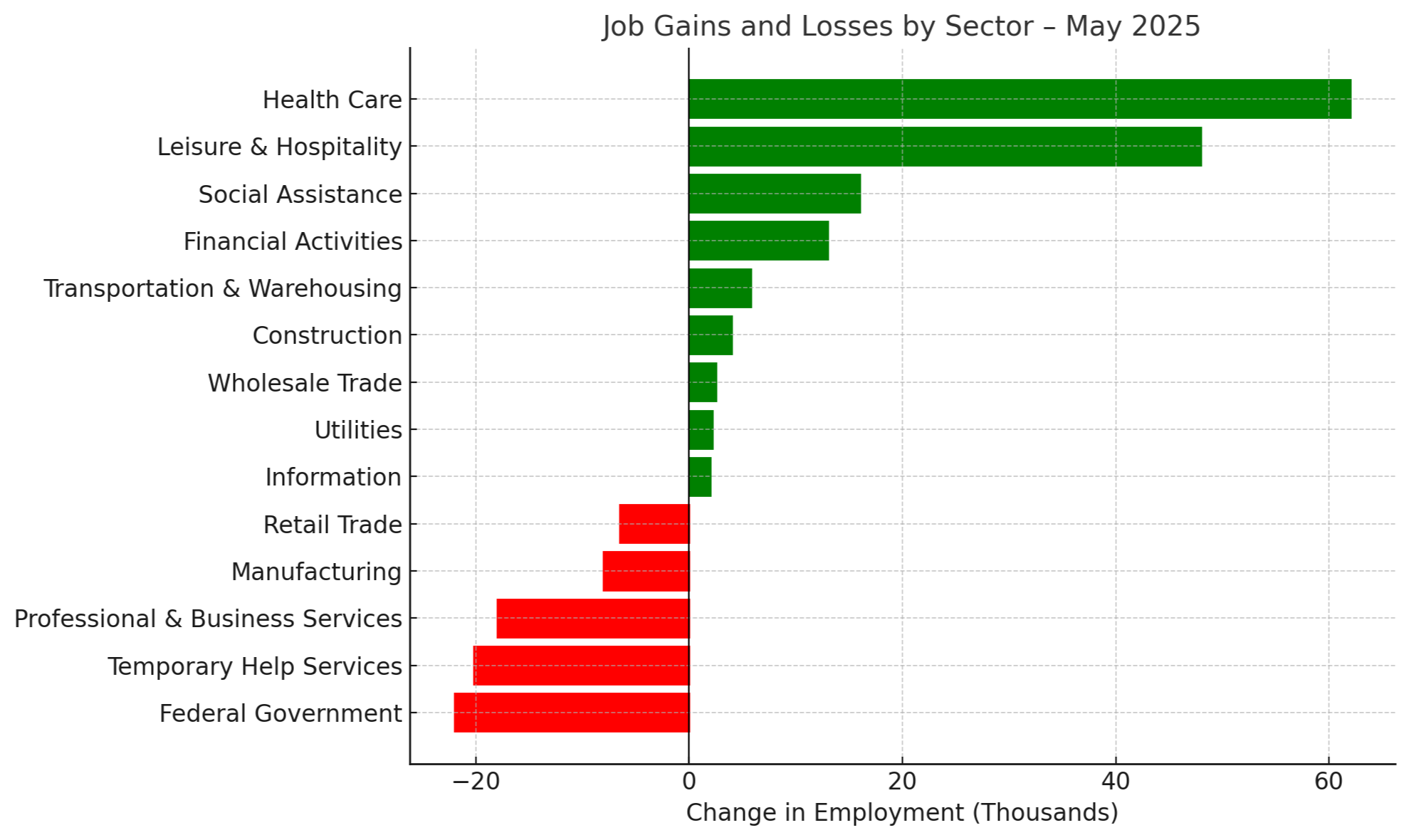

Economy

Friday's jobs report showed continued resiliency in the labor market. In May, 139,000 net new jobs were added to the economy, and the unemployment rate remains unchanged at 4.2%. The downside is the prior two months of jobs reports were revised lower by a total of 95,000 jobs. In addition, the number of people who filed for unemployment insurance last week ticked a bit higher from the previous week to the highest level in 2025. Health care added 62,000 jobs while the federal government workforce was reduced by 22,000 positions. The CME FedWatch tool shows a slightly lower chance of more than one rate cut by the end of the year from the Fed compared to last week. The Fed is less likely to cut interest rates if the labor market maintains its strength while inflation remains above their target of 2%. We'll find out more about inflation on Wednesday next week when the Bureau of Labor Statistics releases the May consumer price index report. The Cleveland Fed's forecasting model calls for CPI to rise from 2.3% to 2.4%, with a slight increase on core CPI (inflation ex-food and energy) to 2.84% from 2.78%.

Source: BLS

Markets

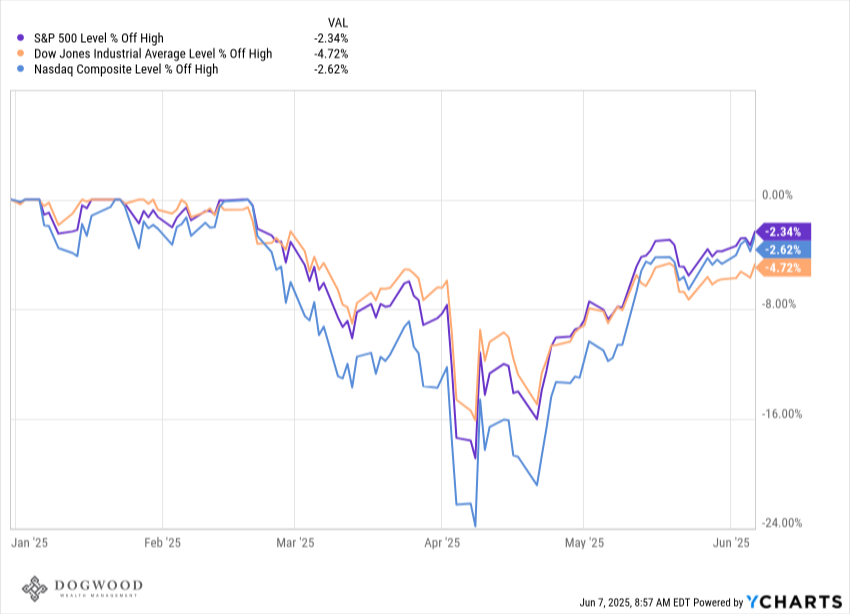

Back-to-back solid weeks for the stock market saw the S&P 500 rise 1.5% for the week of June 2-6. Markets responded favorably to both the May jobs report as well as news that President Trump and President Xi Jinping held a 90-minute phone call to discuss trade policy. Both sides apparently agreed to send representation to meet in London this upcoming meet to discuss a deal. Good enough for the S&P 500 to close above 6,000, a level not seen since February earlier this year. The index is just 2% from the all-time high after a remarkable turnaround that began just two months ago. In the bond market, treasury rates rose after the strong jobs report with the 10-year climbing to 4.5%. The 20- and 30-year treasury rates sit near 5%.

What We're Reading

Have a great weekend.

Dogwood Wealth Management