Economy

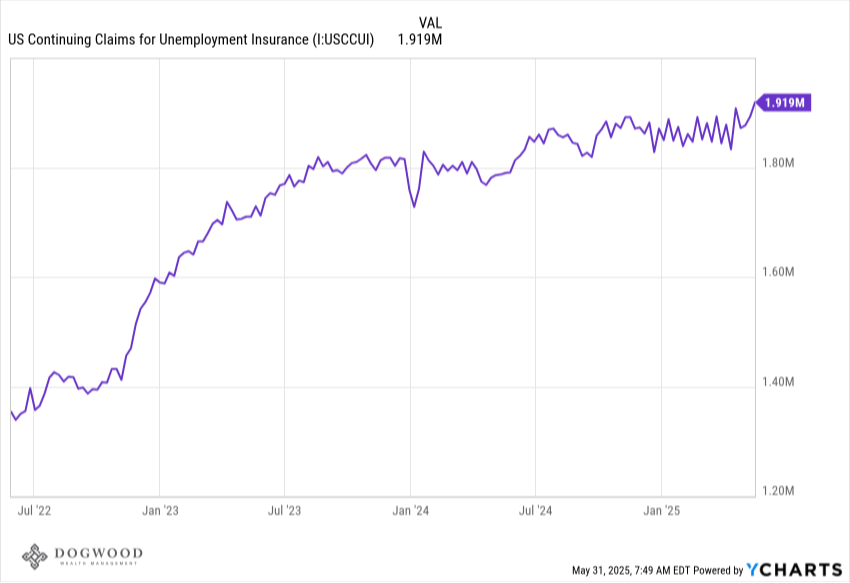

The number of people filing for unemployment insurance last week ticked higher to 240,000, above the 4-week average of 230,075. This is the second reading at 240,000 or higher in the last 5 weeks. The number of continuing claims for unemployment insurance came in at 1.92 million, the highest level since 2021. Claims for unemployment insurance has historically been one of the earliest indicators of a slowing economy, so these figures are worth paying attention to. The Fed is certainly concerned with the labor market, and we'll get an important report next Friday with the Bureau of Labor Statistic's monthly nonfarm payrolls report which will show how many net jobs were created for the month of May.

On the inflation front, the Fed's preferred gauge is the core personal consumption expenditures price index which came in below expectations. Excluding food and energy, the core PCE stands at 2.5%, slightly higher than the Fed's target of 2%. There are concerns that tariffs will reaccelerate inflation, but it's difficult to predict when the tariffs are on, then off, then made illegal, then appealed and allowed the stand, and so on. The Fed is taking a "wait-and-see" approach with interest rates, and not expected to cut rates in a few weeks at the June 18 meeting.

Markets

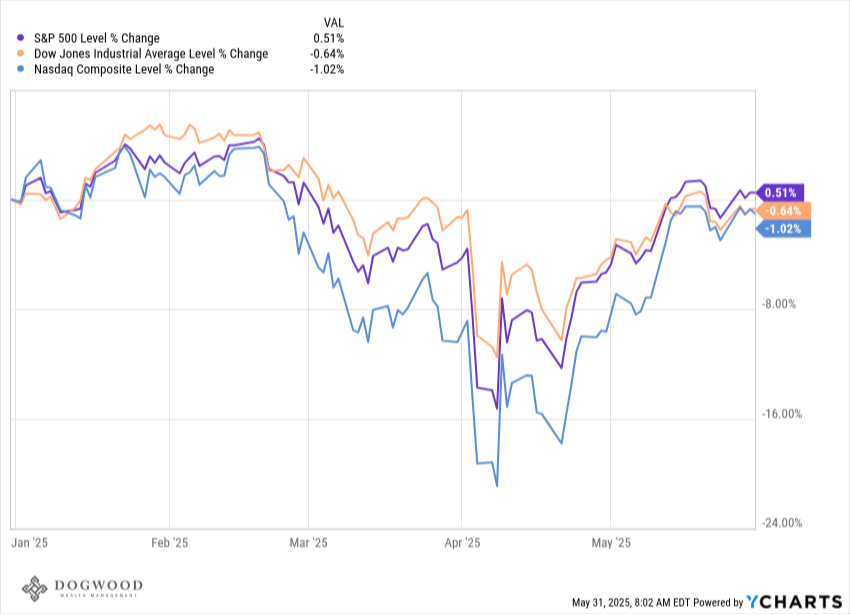

A good week for stocks with the S&P 500 rising 1.88% and closing out the month of May up 6.2%. Stocks have done well recently as we've seen better-than-expected results from corporate earnings paired with solid economic data and rhetoric around tariffs that has improved over the last several weeks. That last part still has the potential to reintroduce volatility to the markets at any given time, but we've come along way since the early days of April. We're entering in to a period where corporate earnings reports for Q1 are behind us, and we're about a month away from the next round of earnings season. This is a time where the market can be driven primarily by macroeconomic events and narratives and less by corporate performance. One of the big narratives out there is growing concern around the national budget deficit. That's had a big impact on rising rates on longer term treasuries recently, leading to higher borrowing costs on not only our national debt but on mortgages as well. Higher rates on longer treasuries can also provide downward pressure on the stock market at some point as it becomes a competing asset class. If the 10-year treasury were to get up to a 5% yield (which briefly happened back in the fall of 2023), bonds look more attractive than stocks, which can lead to a stock market selloff (the S&P 500 fell 10% in the fall of 2023 before rates swiftly fell back down).

What We're Reading

- The West is Trying to Escape China's Grip on Rare Earth Metals - CNBC

- Almost Every Financial Planning Decisions Requires Judgement - Mike Piper

Have a great weekend.

Dogwood Wealth Management