Economy

There was a lot of economic data released this week, and as usual it was a mixed bag. Let's start with the gross domestic product (GDP) report. Economists had expected that the economy would have grown slightly in the first quarter. The consensus estimate was an increase of 0.4%, which would have been down significantly from the previous three readings of 2.4%, 3.1%, and 3%. The number we got was -0.3%. Bear in mind that a recession is loosely defined as two consecutive quarters of negative GDP, and there have been a lot of pundits calling for recession lately. On its face this GDP report would be an outright disappointment. However, one of the components of how GDP is calculated is net exports. If we import more than we export, that can have a negative drag on the GDP number, and that's exactly what happened in Q1. In fact, there was a record surge in imports as companies tried to get ahead of the looming tariffs. All that to say, the negative GDP report may not be as bad as the headline suggests.

Turning to the labor market, we're starting to see the early signs of things slowing down. Every Thursday, the Department of Labor announces how many people filed for unemployment insurance in the last week for the first time, and how many people continue to receive unemployment insurance. The first number (initial claims) jumped this past week up to 241,000 (the average had been around 220,000 for the past several weeks). Perhaps more concerning is the second number, which rose to the highest level since November 2021. Nearly 2 million people are on unemployment insurance today, which suggests those who have been laid off are finding it harder to secure their next job.

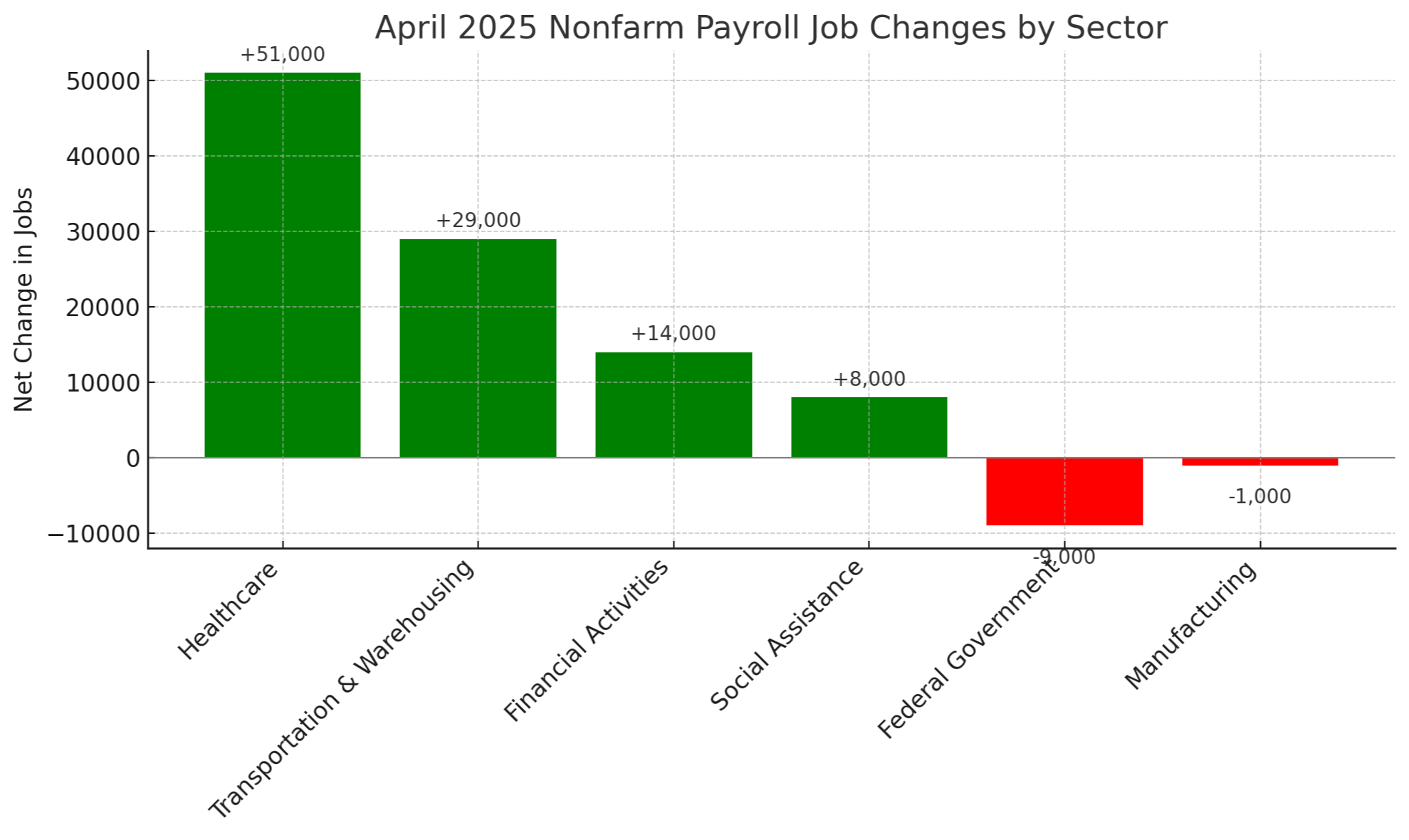

On Friday, the Bureau of Labor Statistics (BLS) released the April jobs report, which showed there were 177,000 new jobs created for the month. The BLS also reports that there are presently just shy of 7.2 million job openings waiting to be filled. The number of jobs created in April was actually more than economists expected by about 40,000. The unemployment rate is 4.2%, which suggests "full employment", or put more plainly, if you want a job, you can find a job (maybe not the job, but a job). Last month, the sectors that saw gains in jobs created were healthcare, transportation and warehousing (possibly linked to the surge in imports due to tariffs?), and financial services. You probably could have guessed that jobs continue to be lost in the federal government. In addition, the report showed that despite the number of jobs created beating expectations, average hourly wages continue to decline.

Markets

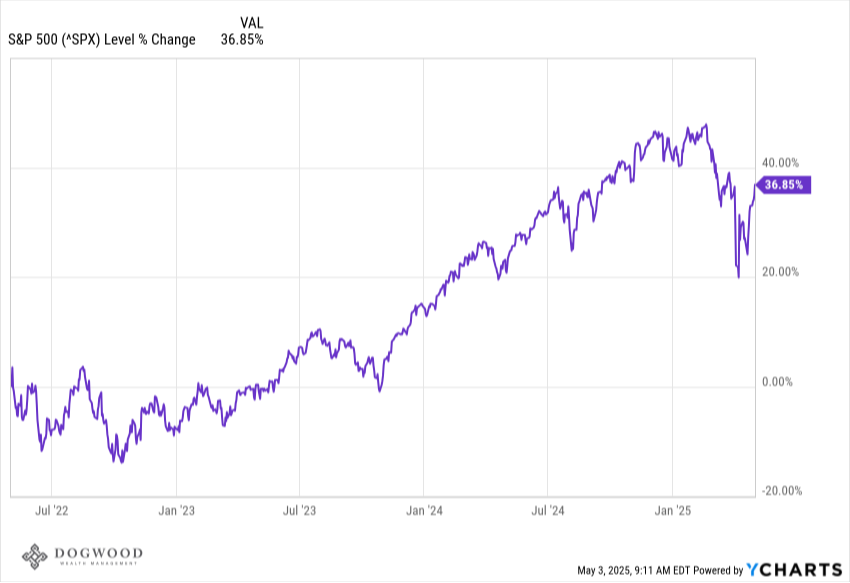

There's been a incredible turnaround in the market. In fact, April was one for the ages. After falling more than 10% in the month of April, the market rallied back up 10% off the lows. The S&P 500 has risen for 9 consecutive days and was up 2.92% last week. We actually closed higher on Friday than the market was when President Trump announced his tariff plans on "liberation day" (April 2). Since that day, there's been a lot of changes on the tariff front in the form of carve outs, supposedly progressing talks with foreign trading partners, and what could be interpreted as the administration softening its stance. That said, it appears the market is somehow able to look past the news of the day. The market doesn't seem concerned with tariffs at this moment. Earnings season is in full swing and the results have been strong. This past week saw four of the magnificent seven stocks beat their earnings expectations. It's not just the Mag 7, either. Small cap companies have matched the performance of their mega cap counterparts lately. The broad participation in the rally is something typically seen in bull markets.

The S&P 500 is now down just 3.3% year-to-date and 7.5% below the all-time high. This isn't a call by us saying the bottom is in and we're clear skies from here. However, it's significant to recall that back in 2022, the market bottomed and started to rally late in the year before the news started to get better. Historically, if you've been on the sidelines waiting for the proverbial dust to settle or for more certainty, you missed out on the rally that oftentimes comes beforehand. Markets are risky, and that's where the risk premium comes into play.

What We're Reading

- Flying Mohawk Searches for Kentucky Derby Miracle - Sportico

- Formula One's Race to Crack America - WSJ

Have a great weekend.

Dogwood Wealth Management