Economy

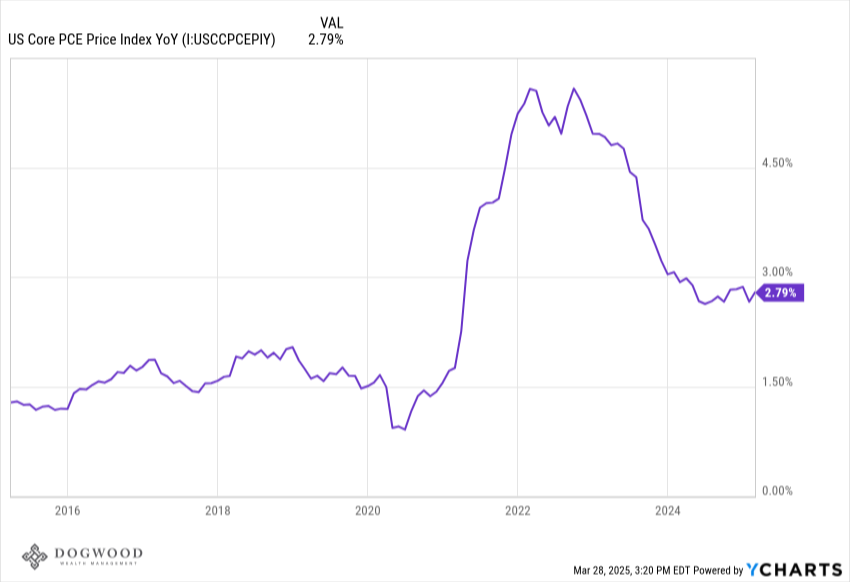

On Friday, the Fed's preferred benchmark for inflation rose slightly more than expected. Their stated target inflation rate of 2% is lower than the current core PCE reading of 2.79%. For context, core PCE in February 2024 was 2.93%, so we really haven't made much progress on that front, which is one of the reasons the Fed is holding rates steady and not cutting further. However, if the economy began to slip, they may have to cut rates sooner than they would like. Jerome Powell reiterated the Fed's plan for one or two rate cuts this year at his last press conference, but the market is betting on three or four by the end of the year. To that point, sentiment on the economy continues to worsen. The University of Michigan's widely followed monthly survey on consumer confidence declined to the lowest level since 2022. The survey reflects consumers' souring outlook on the direction the economy is headed. Respondents expect higher unemployment and higher inflation over the next year.

You may be thinking, "Who's answering this? I've never been contacted by them." You'd have a good point. Never put too much stock in survey data as it can be flawed and useless for crafting an investment strategy. It is, however, arguably an important insight into how people are thinking. If the consensus opinion on the economy is negative, one might extrapolate that to think people may start to think twice about discretionary spending or investment, things that could actually have an impact on the broader economy. Sentiment can turn on a dime, however, so take it with a grain of salt.

Markets

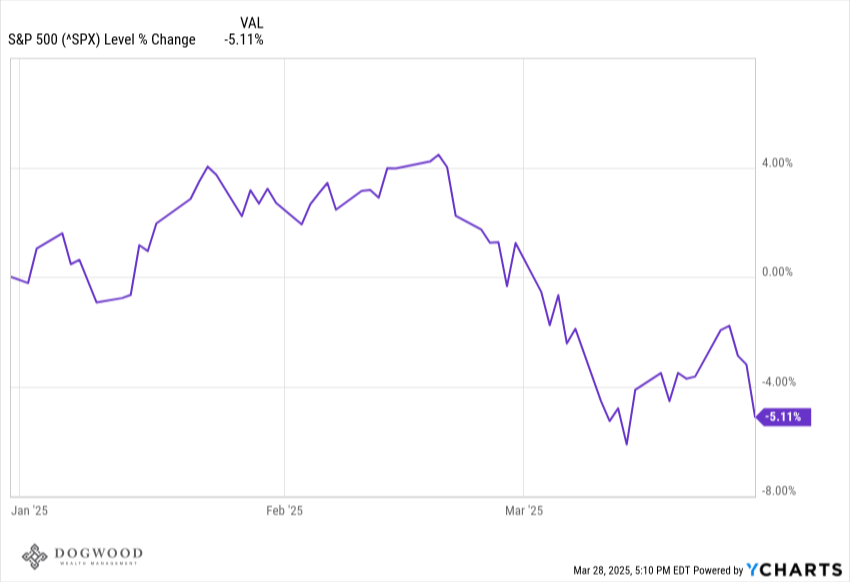

The S&P 500 got off to a hot start Monday as it appeared president Trump may have softened his stance on tariffs. "I'll probably be more lenient than reciprocal, because if I was reciprocal, that would be very tough for people," were his words in an interview this week. In addition, the administration has given a few examples of exceptions to tariffs, although president Trump also said he would try to limit exceptions in that same interview. Still, what his administration is referring to as "Liberation Day" is just around the corner (April 2), and the tariff discussion has had a visible drag on the equity markets over the last month and a half. By the end of the week, Monday's enthusiasm had worn off completely, and the index wound up declining by 1.53%. The S&P is poised for it's worst month since 2022 as this story continues to play out. Nothing happens in a vacuum, but it remains to be seen how consumer sentiment (which is lower in large part due to tariffs) may impact corporate earnings as we move throughout the year. We're a couple of weeks away from getting into Q1 earnings season still, and a lot can change between now and then.

What We're Reading

- What is "Liberation Day"? - CBS News

- Beautiful vs. Practical Advice - Morgan Housel

Have a great weekend.

Dogwood Wealth Management