Economy

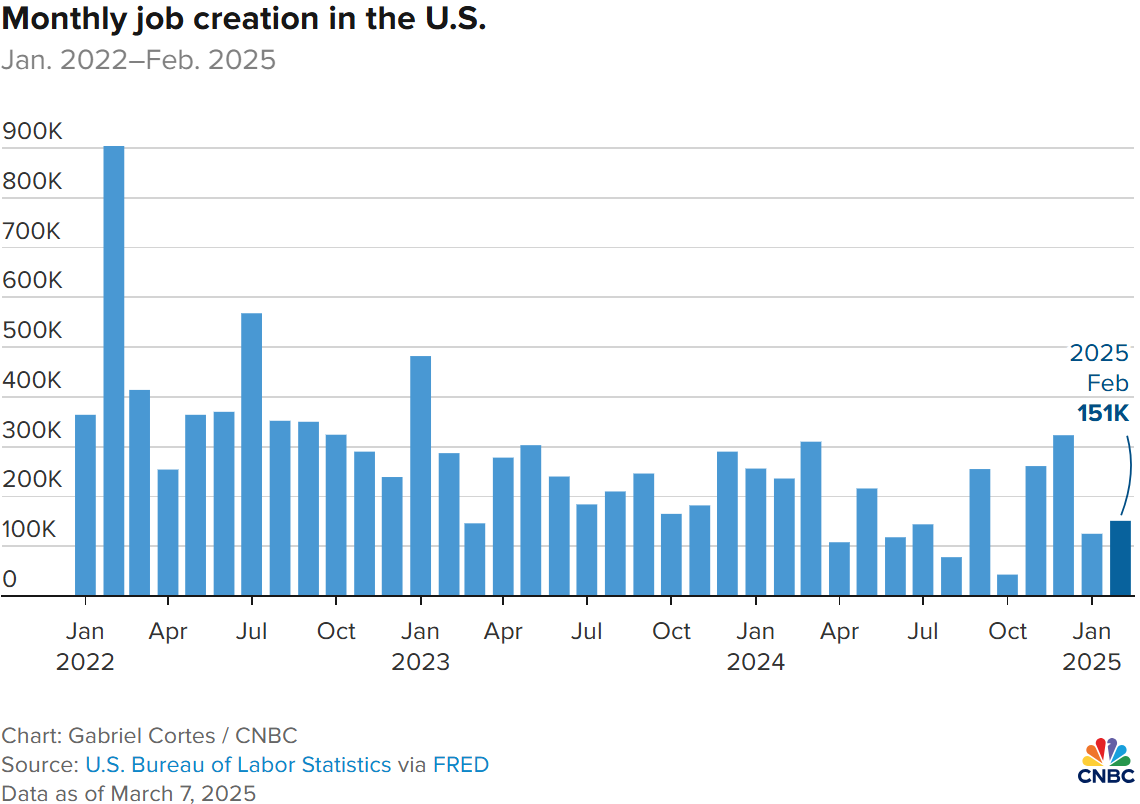

The February jobs numbers came in lower than expectations Friday. Wall Street was looking for around 170,000, but the actual numbers of jobs created in February was 151,000. The January jobs numbers were also revised downward by 18,000 and that was from a number that was originally lower than expected as well. The unemployment rate ticked up to 4.1% from 4%. Federal jobs were cut by 10,000, and that's a number that's likely going to continue to decline in future reports. For the last few years the labor market has been incredibly resilient but in recent weeks has shown some signs of stress.

Markets

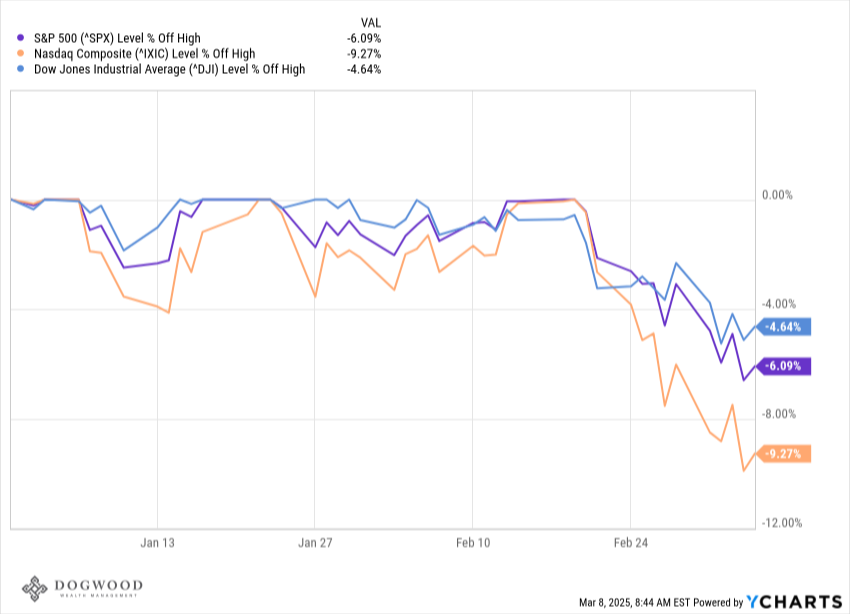

The S&P 500 had its worst week in 6 months falling 3.1%. The index is now 6% off its high point put in earlier this year, which seems like an eternity ago. The tech-heavy Nasdaq entered into correction territory after falling more than 10% from its high water mark. The heavy selling has left sentiment in the toilet.

This wasn't about corporate earnings or economic data. The tariffs on Canada, Mexico, and China were a major development this week. Canada and China immediately responded with tariffs of their own. Then the Trump administration said automakers would get some extension before tariffs kicked in, and later stated that additional imports would see a delay in tariffs for a month if they were compliant with the USMCA trade pact. It's hard to know exactly what the stated goal of the tariffs is right now. The administration has given a few reasons including curbing fentanyl, illegal immigration, and the trade deficit. Without specifics, it's difficult to know how this tariff chapter will play out. It's a fluid situation that could drag on, but could also be over with after a late night post on Truth Social.

The administration has admitted that they are willing to tolerate a bit of short-term damage the markets and the economy to accomplish their broader goals of border security and addressing the trade deficit, things that they hope would leave us in a better place when we come through to the other side. Because the recent market volatility is somewhat self-inflicted, therein lies the case for the optimist. President Trump used the stock market as a scoreboard during his first term. There is a case to be made that if he is looking at the market to be a barometer of success, he has some ability to "save" the market should he choose to do so by backing off the tariffs. On the other hand, he's not running for reelection this time, and some comments from this administration have suggested the market is secondary to their broader goals.

Then there's also Jerome Powell, who hasn't been in the headlines lately with everything going on. Interest rates are higher today than the first Trump administration. The Fed was also raising rates back then, and is currently several months in to a rate cutting cycle. The ability of the Fed to provide stimulative rate cuts could provide some relief to the stock market if things start to get real ugly. While Powell hasn't said or done anything to suggest this would happen (partly because he hasn't had the opportunity to do so), Wall Street has started to price in an increased number of rate cuts by the Fed in 2025.

What We're Reading

- Stock Market Crashes: A Look at 150 Years of Bear Markets - Morningstar

- The Walgreens Billionaire Watching His Empire Come Apart - WSJ

Have a great weekend.

Dogwood Wealth Management