Economy

Let's start by addressing the tariff story concerning Mexico, Canada, and of course China. The Mexico and Canada story began late last week and came to a close (or did it?) a few hours into trading on Monday. For now, it appears there's been a reprieve for a month, but truth be told this may be a developing story that has lots of twists and turns. If you're a Chiefs fan and have been watching their games this season, you're used to this "edge-of-your-seat" feeling. For now, you're probably safe (and better off) to ignore the tariff stories. Tariffs might have an economic impact should they materialize, but until more is known, let's leave that to the speculators.

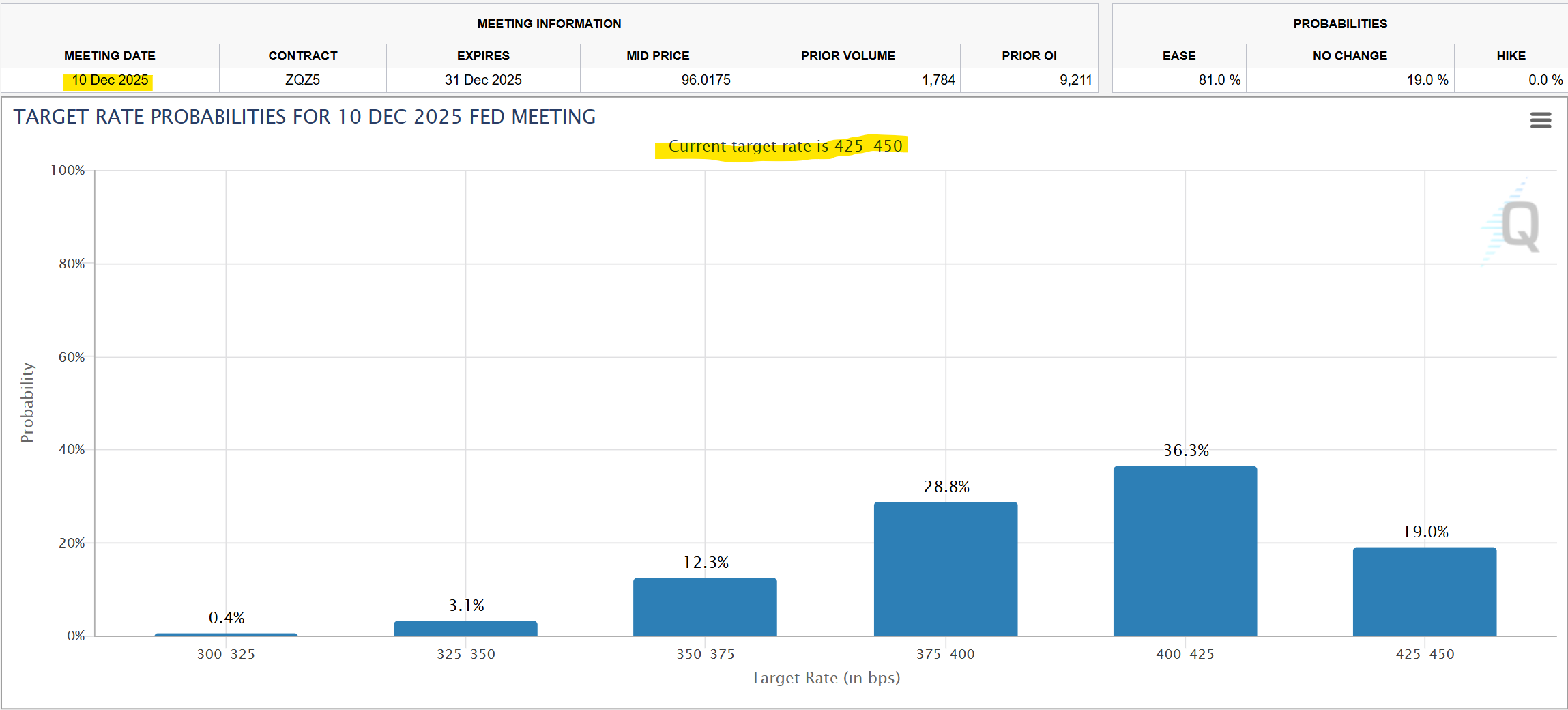

Perhaps more significant, there were a few labor market-related reports out this week. First, weekly claims for unemployment insurance remained fairly subdued this week, rising slightly off a fairly low number last week. Second, while the January jobs report showed fewer jobs were created that expected (143,000 vs 169,000), the unemployment rate ticked lower to 4%, and the number of jobs created in November and December were revised upwards by 100,000. Both reports suggest the labor market remains on solid ground. Wages rose more than expected in January but the Fed has repeatedly stated they are not worried that wage growth is a major contributor to inflation. Right now, the market is pricing in about a 50/50 chance of a rate cut at the June Fed meeting, and about a 50% chance we see more than 1 rate cut by the end of the year.

Source: CME Group (https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html)

Markets

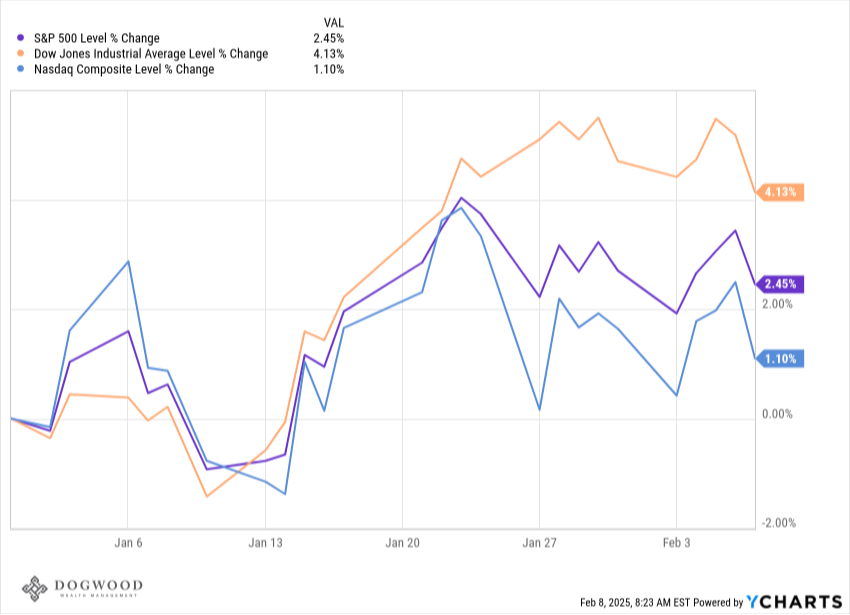

Can we get a "normal" Monday next week, please? The markets opened in a panic for the second consecutive week. This time it wasn't a Chinese AI company, but tariffs threw the markets in a chaotic mess. The Dow at one point was down 665 points early Monday before the news broke that President Trump had spoken with President Sheinbaum of Mexico, and later Prime Minister Trudeau. The market recovered nearly all of these early losses by Monday's close, and finished the week down just 0.24%. The tariff sideshow aside, corporate earnings continue to come in strong for Q4 as companies are reporting above-expected results at an above-average rate. Between solid economic data and strong earnings growth, we continue to be optimistic on the market. However, recently we've seen a few examples of how markets can have volatile reactions to day-to-day headlines despite the overarching trend.

What We're Reading

- Older Is Better - WSJ

- Be Water, My Friend - Tony Isola

Have a great weekend. Go Chiefs!

Dogwood Wealth Management