The recently passed tax legislation marks one of the most sweeping overhauls to the U.S. tax code since the 2017 Tax Cuts and Jobs Act (TCJA). While some provisions extend popular elements of the TCJA, others introduce entirely new concepts aimed at workers, families, and business owners. Below, we’ve summarized the key changes taking effect in 2025 and those scheduled to begin after that. Whether you're a high-income earner, a retiree, a small business owner, or just trying to make sense of what’s coming, these updates are worth understanding.

Tax Changes Going Into Effect in 2025

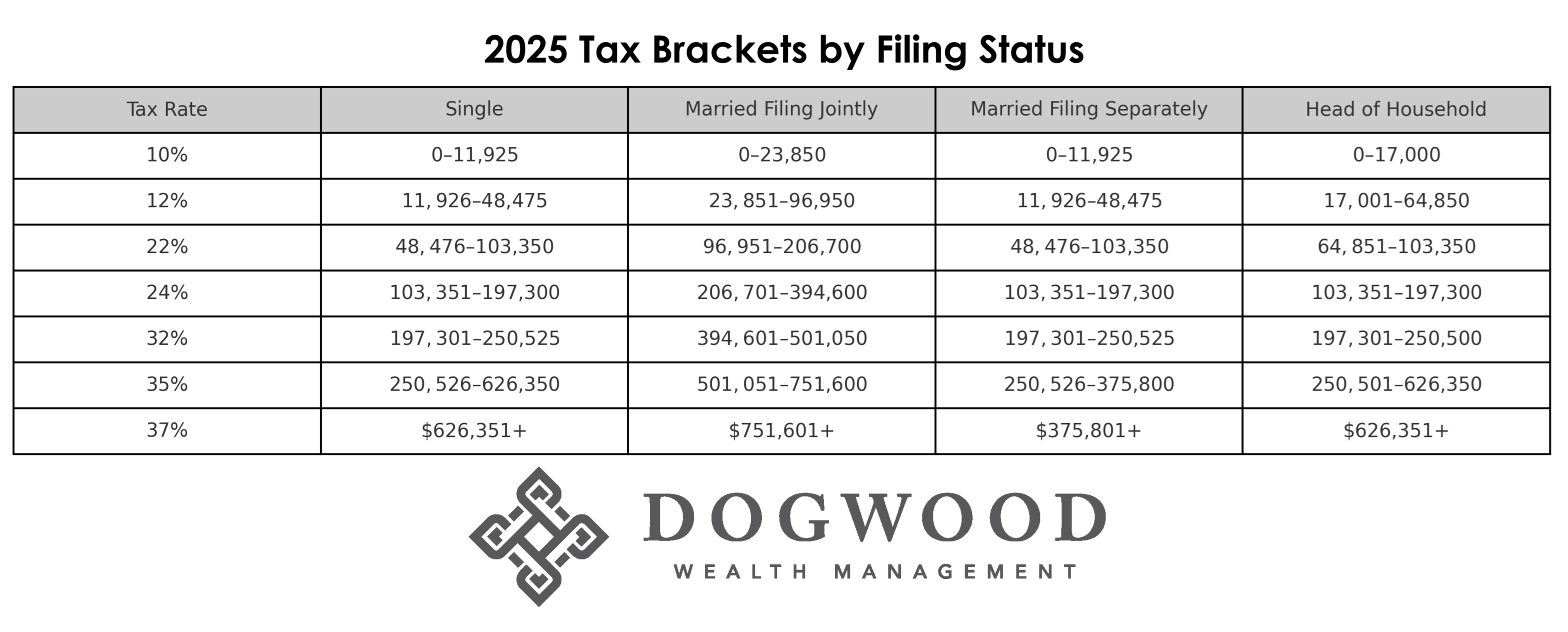

Income Tax Brackets Made Permanent

The ordinary income tax brackets ranging from 10% to 37%—initially set to expire in 2026 under the TCJA—have now been made permanent. These brackets will continue to be indexed for inflation, providing some long-term clarity and planning potential for taxpayers.

Itemized Deductions Get a Tune-Up

The Pease limitation, which previously reduced itemized deductions for high-income earners, is permanently repealed.

Miscellaneous itemized deductions remain eliminated, meaning taxpayers still cannot deduct expenses like unreimbursed employee expenses or tax prep fees.

The mortgage interest deduction cap remains at $750,000, though some mortgage insurance premiums (MIP) will now be deductible again in limited cases.

Personal Exemptions

No change here—personal exemptions remain eliminated, continuing the status quo from recent years.

ABLE Accounts Expanded

Contributions to ABLE (Achieving a Better Life Experience) accounts will continue to:

Qualify for the Saver’s Credit

Accept rollovers from 529 college savings plans

These accounts remain an excellent tool for individuals with disabilities to save in a tax-advantaged way without affecting eligibility for government benefits.

Tax-Free Student Loan Assistance

Employers can continue to contribute up to $5,250 annually (indexed for inflation) toward employees’ student loans tax-free. This provision, once considered temporary, is now permanent.

Excess Business Loss Limitation

The limit on excess business losses for non-corporate taxpayers has been made permanent, preventing large write-offs against non-business income.

SALT Cap Increased

One of the most notable updates: the state and local tax (SALT) deduction cap increases to $40,000 for joint filers ($20,000 if married filing separately), phased out between $500,000 and $600,000 in AGI. This provision is indexed at 1% annually and applies from 2025 through 2029.

Qualified Business Income (QBI) Deduction Extended

The popular 20% deduction for pass-through business income (e.g., S corps, partnerships, sole proprietors) is now permanent, with several enhancements:

The phaseout range has been widened

A new minimum deduction of $400 is added for qualifying filers

New Above-the-Line Deductions for Workers

A few new deductions arrive under what some are calling “below-the-below-the-line” deductions:

No Tax on Tips: Up to $25,000 in tip income can be deducted (except for married filing separately), phased out for high-income earners. Applies from 2025–2028.

No Tax on Overtime: Overtime pay is deductible—up to $12,500 (or $25,000 MFJ)—for 2025–2028.

Auto Loan Interest: Up to $10,000 in auto loan interest is deductible for qualified U.S.-assembled vehicles, phased out based on income.

Standard Deduction Increased

The standard deduction jumps to:

$31,500 for married filing jointly

$15,750 for single filers

$23,625 for heads of household

Senior Deduction Introduced

Taxpayers aged 65 and older can now deduct an additional $6,000 above the line, though this is phased out for high earners. This deduction runs from 2025 through 2028.

Child and Adoption Tax Credits Expanded

The Child Tax Credit increases to $2,200 per child, with permanent inflation indexing.

The Adoption Credit becomes refundable, with a cap of $5,000 starting in 2025—an important change for families adopting children from foster care or abroad.

Section 179 Expensing and Bonus Depreciation

Section 179 expensing is increased to a $2.5 million cap, phasing out at $4 million. This allows businesses to write off qualifying equipment purchases more easily.

100% bonus depreciation returns for property placed in service on or after January 20, 2025, making it easier to fully deduct major investments in year one.

New “Trump Accounts” for Minors

A new type of savings vehicle is being introduced:

Up to $5,000/year in nondeductible contributions for those under age 18

Employers may contribute up to $2,500

An IRS pilot program will provide a $1,000 seed credit for children born from 2025–2028

Provisions Taking Effect After 2025

Non-Itemizer Charitable Deduction

Starting in 2026, even taxpayers who don’t itemize can deduct up to:

$2,000 for married filing jointly

$1,000 for others

This aims to broaden charitable giving incentives.

Charitable AGI Floor for Itemizers

For itemizers, a 0.5% AGI floor applies beginning in 2026—meaning deductions for charitable giving must exceed that threshold to count.

AMT Exemption Phaseout Resets

Beginning in 2026, the Alternative Minimum Tax (AMT) exemption begins phasing out at:

$1 million for joint filers

$500,000 for single filers

This reverts AMT treatment closer to pre-TCJA levels for high earners.

Estate and Gift Tax Exemption Increased

Starting in 2026, the estate and gift tax exemption increases to $15 million per person, adjusted for inflation. This may prompt revised estate planning strategies for ultra-high-net-worth families.

Final Thoughts

This new legislation presents a blend of permanence and phase-in. While many TCJA-era provisions are locked in for the long haul, the next few years offer unique opportunities for proactive planning. For example, taxpayers may want to:

Bunch charitable contributions before the AGI floor hits

Adjust pass-through entity compensation in light of QBI changes

Consider estate strategies before the new exemption kicks in

As always, we recommend reviewing your situation with a qualified tax advisor to identify which changes apply to you and how best to navigate them. If you're a Dogwood Wealth Management client, reach out—we’re ready to help you plan strategically around these updates.